Role: Sole Designer & Developer

Team: Solo Project

Tools Used: Figma

Duration: Started 3 Months ago, ongoing

Platform: Android / iOS

Overview

When I got my first job in high school, I pretty much spent everything every time it was pay day. At the time, being a high schooler it feels like you can buy anything your heart desires, it was an amazing feeling. I eventually started to realize and learn about how to budget and invest your money while in a business class in high school. That class and my teacher completely changed my perspective on money. At the end of high school and after, I read and learned so much about investing, budgeting, and how to build wealth.

For some time, I’ve been looking for a proper budgeting app. I have always just used mental notes on my spending and just tried to spend less than what I make but nowadays that just doesn’t cut it. I’ve looked all over online and asked many friends how they managed to track their spending and found nothing practical.

Now some online banks are more intuitive and user friendly in order to make investing and tracking finances easier. But unfortunately, when you have multiple accounts and lots of transactions coming in and out, it can be difficult to keep track of multiple apps.

I’ve looked around for some apps that can help with budgeting but simply could not find anything fully featured and not cost a ton! Why would I spend over $10 a month just to keep track of my own money!

During my time at the Mobile Design and Development program at Algonquin, I decided to just take the matters into my own hands. That’s when I came up with the idea of Numo Budget.

I decided to create my own budgeting app that is fully featured to be user friendly and allow people to track their spending easily.

Problem Discovery & Research

Project Overview

Numo Budget is a mobile budgeting app designed for a generation of individuals who want a better way to manage their money. The app provides a clean, user-friendly experience that makes tracking expenses, setting financial goals, and visualizing progress easy and stress-free. Built with simplicity, automation, and accessibility in mind, Numo Budget helps users develop healthy financial habits—without feeling overwhelmed.

User Research Summary

In order to conduct my user research effectively and efficiently, I created an anonymous google forms survey that I spread around. I made the form to ask potential users what they budgeting habits look like and what would work for them or not.

The survey was completely anonymous and consisted of 13 questions. Here is the link.

This survey got a surprising 30 responses from different people! Most were aged 18-30, primarily full-time workers, and students.

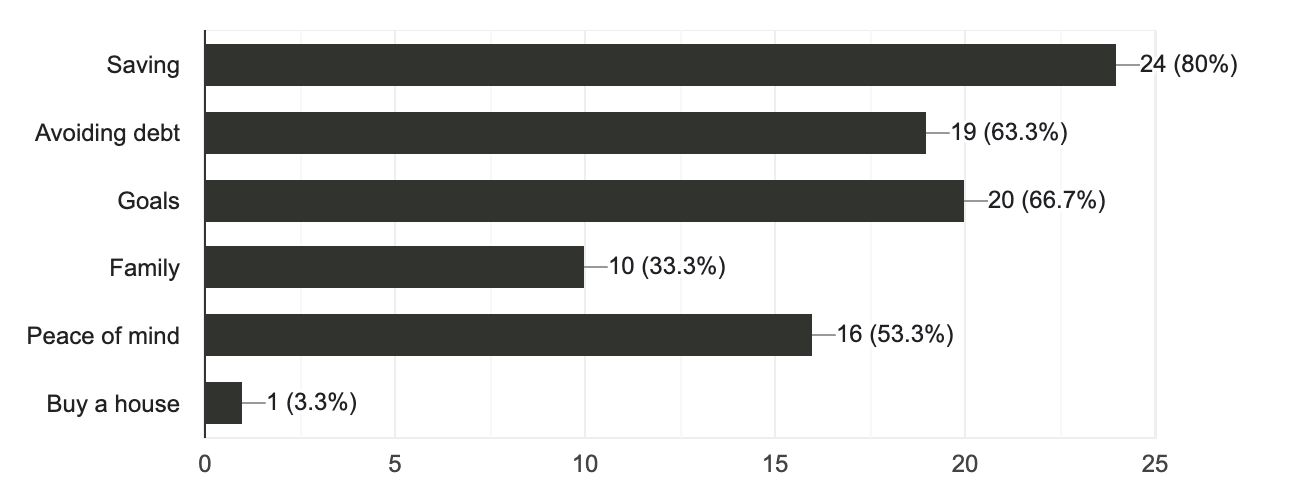

Some key insights I found were that most responders say that they don’t budget or barely do. Over 50% of them said they don’t use anything, rely on memory, or pen & paper.

Respondents also seemed to be frustrated by paywalls, it seems that tools are feeling overwhelming and clunky while also being behind a subscription. This is all based on the responses I got.

I asked questions regarding what motivates these users to budget or even consider using a budgeting tool and it seems like saving, having goals, and a peace of mind are the keys to most users. Emotional drivers such as family, fear of debt, and future planning were strong.

Irregular income also seems to be the situation for just under half of respondents. This must make budgeting harder for some users and will definitely be a big consideration during the design process.

Some of the top desired features include:

- Spending notifications

- Visual stats (graphs, breakdowns)

- Bank syncing and automation

- Simplicity of the UI and clear explantions

From my questions, I wanted users to paint me the picture of how they want budgeting to feel and these are some key direct quotes from the open feedback:

Less stressful.

Not overcrowded.

A more approachable and simple user friendly app.

I would like to see how many days I went without spending so that I can feel good when rewarding myself.

Gamification, points if hit milestones.

Simplicity and a sense of less urgency (Some apps put too much pressure on your bills and debts and make it feel like you have no money at all).

Not looking at the BIG PICTURE all the time & aforementioned automation

I also asked users to explain to me what frustrates and pains them about budgeting apps/tools.

Hard to manage as a student who has so many sudden expenses.

Not streamlined with my bank, over complicated.

They can get too technical or complicated, or they don’t support multiple incomes or incomes for side jobs.

Bank integrations, poor attempts at ai categorization

They’re to help you budget but cost a lot.

Lack of ease or practicality in the UI, lack of automation.

Some great feedback that really stood out to me was the idea of gamification and having budget that goes unspent to be considered for your stats. I like these ideas and it has definitely opened my mind to a more fun approach to saving for users to not feel the dread that comes with thinking of finances.

Overall, all the feedback and responses received have been extremely valuable to me and this research, I am proud of how much data people were willing to share for the sake of the project to create something great.

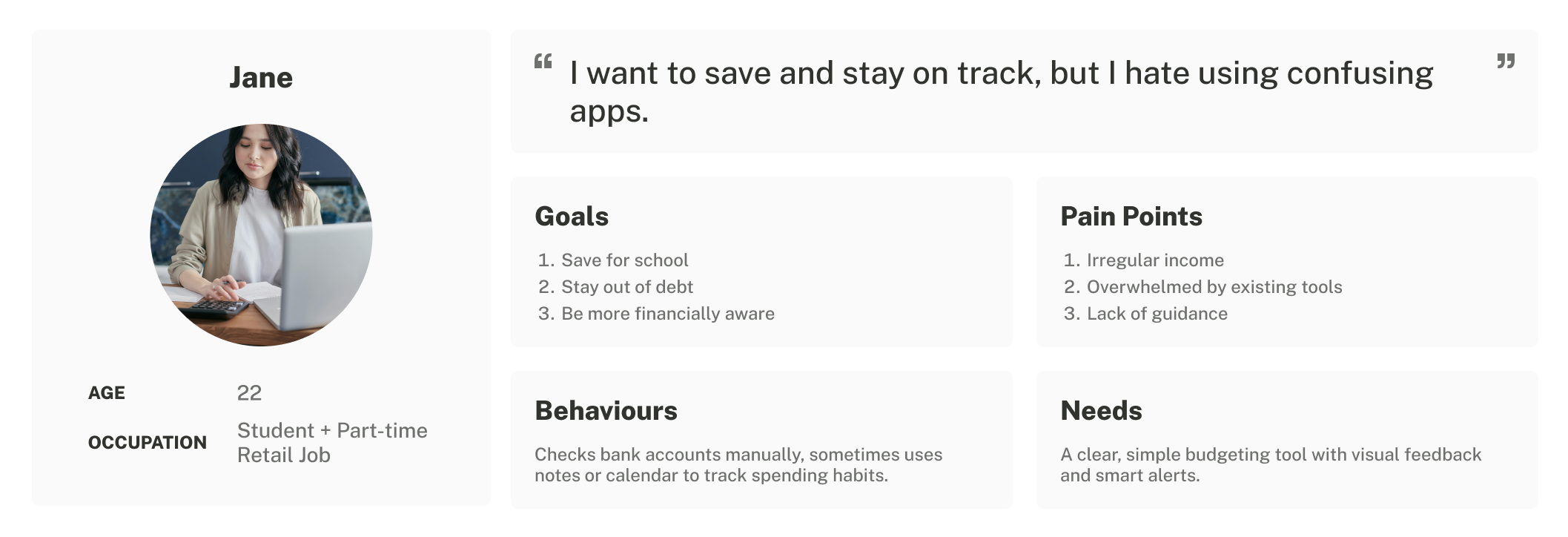

Persona Snapshot

Competitive Analysis

Monarch Money

| What They Do Well | Where They Are Lacking |

|---|---|

| Holistic financial overview with account integrations and dashboards | Premium pricing model; no long-term free version |

| Clean, user-friendly UI with strong onboarding experience | Limited credit score tracking support |

| Strong goal-setting tools with infinite goals and personalized financial insights | Recurring transaction system is clunky and inconsistent |

| Great for couples; supports joint financial planning | Limited reporting tools compared to Mint (e.g., breakdowns, net worth trends) |

| Offers proactive financial advice and insights based on user behavior | Investment tracking is buggy and less reliable than competitors |

| Slow feature development and user-requested updates not prioritized | |

| Difficulties with multi-item Amazon purchases; no auto-categorization |

YNAB (You Need A Budget)

| What They Do Well | Where They Are Lacking |

|---|---|

| Master of zero-based budgeting with behavior-change focus | Steep learning curve for new users unfamiliar with YNAB’s methodology |

| Strong educational materials and community support | No bill tracking or integrated bill pay |

| Excellent sinking fund support and budget flexibility | Lacks comprehensive financial health tools (e.g., net worth tracking) |

| Behavioral rules (“Give every dollar a job,” etc.) that encourage proactive planning | No proactive alerts for unusual account activity |

| Flexible adjustment between budget categories | Email-only support; slow resolution for urgent issues |

| Recent UI updates disliked for being cluttered and less intuitive |

Buddy

| What They Do Well | Where They Are Lacking |

|---|---|

| Manual transaction entry for users who prefer control or enhanced privacy | Frequent bank sync issues; unreliable automatic tracking |

| Supports various pay schedules (weekly, bi-weekly, etc.) | Budget totals and bank balances may show discrepancies |

| Attractive, clean UI with personalized category icons | Customer support often slow or unresponsive |

| Shared budgeting tools for couples/families | Only 7-day trial; not enough time to evaluate syncing reliability |

| Custom category creation with visual customization | Duplicate transaction bugs reported by multiple users |

Budget Bestie

| What They Do Well | Where They Are Lacking |

|---|---|

| Digitally replicates cash-stuffing method for envelope budgeting | No bank integration; all input must be done manually |

| Flexible budgeting cycles based on custom pay schedules | No investment, credit, or net worth tracking features |

| Personalized savings suggestions based on spending behavior | Users can’t easily delete or edit envelopes unless emptied first |

| Hands-on approach helps reinforce budgeting habits | Subscription needed for full access; limited free tier |

| Simple, beginner-friendly design | Occasional crashes and minor bugs reduce trustworthiness |

| Offers payment reminders and upcoming bill forecasts | Mixed reviews about customer support response time |

Through research based on what competitors are doing, I found what Numo could do differently.

-

Hybrid Connectivity: Offer reliable, optional bank syncing alongside exceptionally fast & intuitive manual entry, catering to diverse user needs.

-

Actionable Visual Reporting: Deliver dynamic, visually appealing charts that go beyond basic data, providing “storytelling” insights and “future impact” projections.

-

Smart Behavioral Nudges: Implement subtle, intelligent prompts based on user habits and goals (e.g., proactive budget adjustments, positive reinforcement).

-

Flexible Budgeting Structures: Master hyper-personalized budgeting schedules that fluidly adapt to any pay cycle, not just monthly.

-

Gamified Progress & Learning: Integrate gamification elements (streaks, milestones, challenges) and contextual help to make budgeting engaging and educational.

Some differentiators that I would want to implement and use in Numo Budget would consist of a very simple and minimal structure while making the user feel at ease with the experience. I want the users to feel they can easily budget and not feel confused or overwhelmed.

The responses I got from users showed me that most users feel overwhelmed and confused when navigating the bigger and more traditional budgeting apps, this is exactly what I am trying to stay away from.

Key Differentiators:

- Simple onboarding for non-budgeters.

- Minimal UI with strong visual feedback (progress bars, colour-coded).

- Friendly tone and feedback that feels like a coach, not a calculator.

- Quick-entry for expenses, no jargon, no bloat.

- Optimized for mobile first — tap, add, done.

Problem Statement

Many young adults and individuals with irregular income struggle to manage their finances due to the complexity, lack of personalization, and poor usability of existing budgeting tools. They need a simple, intuitive way to track spending, set goals, and feel in control of their money; without the overwhelm.